Bill Jones — Insurance content contributor

Shopping for auto insurance shouldn’t feel like guesswork. The top 10 car insurance companies show you the leaders that dominate by size and the carriers that consistently deliver on price, claims, and service.

There isn’t a single “best” car insurer for everyone, but there’s always a best fit for your driver profile, budget, and state. Auto insurance companies considered market-share leaders offer reach and stability , while our “best overall” pick shines in multiple categories.

Top 10 Car Insurance Companies in Detail

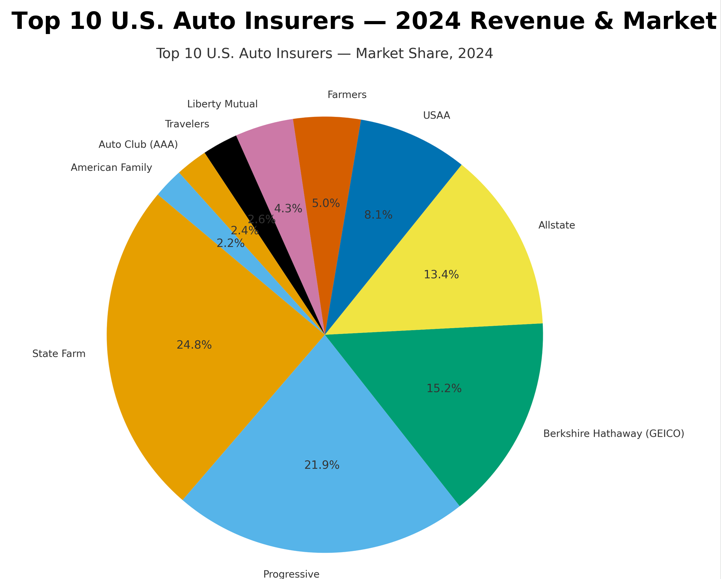

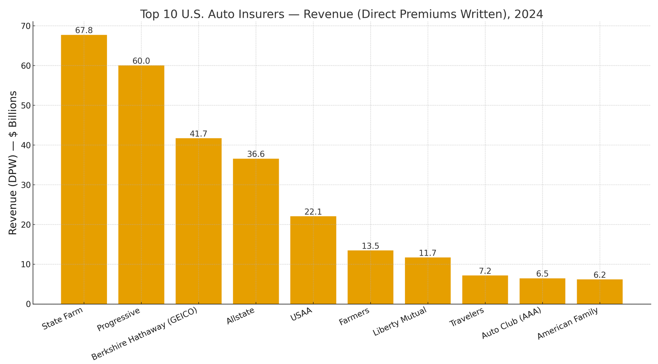

1. State Farm

Preview: The biggest U.S. auto insurer, blending a huge agent network with steady claims support and broad discount/bundle insurance options.

Strengths: National reach; strong agent guidance; deep repair network; family-friendly programs.

Weaknesses: Not always the lowest price; telematics savings depend on your actual driving.

2. Progressive

Preview: Digital-first heavyweight with sophisticated pricing and wide appetite—including higher-risk drivers—plus robust online tools.

Strengths: Strong telematics (Snapshot); excellent quoting/claims UX; big discount stack.

Weaknesses: Snapshot can raise rates for risky habits; prices vary widely by ZIP and profile.

3. Berkshire Hathaway (GEICO)

Preview: App-centric savings leader for many clean-record drivers; fast to quote, easy to manage.

Strengths: Competitive pricing; quick self-service; familiar discounts.

Weaknesses: Limited local-agent support; less forgiving for high-risk histories.

4. Allstate

Preview: Feature-rich national brand with strong agent presence and add-ons that can cushion rate shocks.

Strengths: Options like accident forgiveness/new-car replacement (where offered); solid bundling.

Weaknesses: Often mid-to-high priced; savings vary by state and driver behavior.

5. USAA* (eligibility required)

Preview: Built for military families, with deployment/storage flexibility and member-focused service.

Strengths: Military-tailored discounts; integrated banking/insurance; consistent service reputation.

Weaknesses: Eligibility gate; still smart to benchmark a civilian carrier.

6. Farmers

Preview: Agent-guided coverage with practical endorsements; good fit for households wanting hands-on help.

Strengths: Personal agent advice; useful add-ons; solid everyday discounts.

Weaknesses: Not as price-aggressive as direct writers; telematics/app depth can lag leaders.

7. Liberty Mutual

Preview: Big-name flexibility with endorsements (e.g., new/better-car replacement) and both digital and agent channels.

Strengths: Broad availability; customizable coverages; decent online tools.

Weaknesses: Pricing can skew higher without strong bundles/UBI results; service varies by region.

8. Travelers

Preview: Balanced national carrier with many ways to save, multiple telematics paths, and forgiveness options for price stability.

Strengths: Wide discount lineup; choice of short-trial or ongoing telematics; accident/minor-violation forgiveness.

Weaknesses: Telematics may raise or lower renewal pricing; features vary by state.

9. Auto Club Enterprises (AAA)

Preview: Insurance plus AAA membership perks and roadside—appealing if you value bundled benefits and local club service.

Strengths: Integrated roadside; strong agent presence in club territories; membership value.

Weaknesses: Pricing/availability vary by club; membership fees; not always the cheapest coverage with the lowest deposit.

10. American Family

Preview: Agent-backed coverage with modern telematics, especially strong in Midwest/Western states and family policies.

Strengths: Two UBI options (comfort-level choice); teen-friendly discounts; solid home/auto bundles.

Weaknesses: Regional footprint; UBI savings and rules differ by state and driving behavior.

Best Overall Insurer

If you want one carrier that balances price, coverage depth, and day-to-day usability across most states, Travelers is our best overall pick. It combines broad national availability with a deep discount menu (bundling, safe driver, multi-car, homeowner/affinity, EV/hybrid) and flexible telematics through the IntelliDrive family. This way, you can choose a short trial or an always-on program.

Add optional accident and minor-violation forgiveness, and Travelers helps keep costs predictable after a slip-up. Digital tools are solid, yet you still have access to human help when you need it. For the best price, quote it with identical limits/deductibles, enable paperless/autopay, and test telematics if you’re a smooth, low-mileage driver.

How To Find The Best Auto Insurer With The Best Rates

- Decide coverage first. Pick your liability limits, deductibles, and must-have add-ons (gap/loan-lease, new-car replacement, OEM parts, rideshare, roadside).

- Quote three to five carriers. Start with one brand from your situation above (teens, seniors, discounts, military) and add two or three big nationals from the top 10 car insurance companies list for price context. Use the same limits and deductibles for all quotes.

- Try telematics if you’re a good candidate. Low mileage, daytime driving, and smooth habits usually do well. If you regularly drive at night, brake hard, or use your phone while driving, skip it.

- Weigh service vs. savings. If frictionless claims matter most, prioritize Amica and Erie (where available) and add Travelers or State Farm. If savings matter more, compare Nationwide, Progressive, GEICO, and Travelers with a telematics trial.

- Re-shop annually or after life changes. Moving ZIP codes, adding a teen, changing vehicles, or mileage shifts can reshuffle your best-price order.

What Insurers Are Best For?

Best Two For Teens

State Farm

American Family

Best Insurers For Seniors

Amica

Erie

Best Two Car Insurance Companies For Discounts

Nationwide

Travelers

Best for Military Members

USAA

FAQs

State Farm typically holds the largest private-passenger auto market share nationally. Remember: “largest” reflects premiums written, not necessarily the best fit for your profile.

“Largest” is about market share and reach. “Best” weighs things like claims experience, customer satisfaction, complaint levels, financial strength, coverage options, and price. The ideal pick balances both access and experience for your situation.

State Farm and American Family are strong starts because they pair teen-friendly discounts with coaching/telematics programs that reward safe habits. Their agent support also helps parents set coverage and expectations.

Amica and Erie are popular with long-time drivers who value smooth claims, steady communication, and predictable pricing features (where available). They’re excellent when frictionless service matters more than chasing the absolute lowest quote.

Nationwide (behavior-based and pay-per-mile options) and Travelers (broad discount menu plus forgiveness features in many states) give households multiple paths to durable savings without sacrificing big-carrier stability.

USAA should be your first quote if you’re eligible. It’s built around military life with deployment/storage options and service tuned to PCS moves and documentation needs. Still get one civilian quote to benchmark.

No. Telematics can reduce your rate if you drive smoothly, mostly during the day, and cover fewer miles. Aggressive braking, late-night driving, and phone distraction can limit or negate savings. Review rules and consider a trial before committing.

Pull three to five quotes using identical limits and deductibles. Re-shop yearly or after life changes (move, new driver/vehicle, big mileage shifts, at-fault accidents dropping off). Pricing order can flip even with small changes.

Start with higher liability limits than state minimums (e.g., 100/300/100 or better), then add collision/comprehensive if your car is newer or valuable. Consider gap/loan-lease coverage for financed vehicles, OEM parts for late-model cars, and rideshare coverage if you drive for an app.

Ensure everyone’s safe, call authorities if required, document the scene (photos, details, witnesses), notify your insurer promptly, and keep receipts for related expenses. Stick to the facts, respond quickly to adjuster requests, and choose a repair facility you trust (or a network shop if you want streamlined billing).

Conclusion – Choosing From The Top 10 Car Insurance Companies

There isn’t a single “best” car insurer for everyone, but there’s a best fit for your driver profile, budget, and state. The market-share leaders offer reach and stability, while our “best overall” pick shines in claims, price, and customer service. Use the detailed information above to get matched with an insurer that fits your specific situation.

Bottom line: set your coverage and create a shortlist of three to five carriers from this Top 10 list, and compare apples-to-apples quotes. Then, choose the policy that balances cost, coverage, and claim confidence. Then get all the discounts you can to save the most.

Compare quotes online from the top 10 car insurance companies and save more with direct rates.